Personal Finance for Young Professionals

Jesse Chen • April 3, 2013 • 16 min read

One of the most valuable classes at Cal that I attended was not an engineering class, nor was it technical. It was UGBA 196, Personal Financial Management. Professor Selinger seared into our brain about "the magic of compounding" and how it is ever so important that managing your personal finance while you are still young will reap benefits orders of magnitudes higher than if you started later.

I'm writing this guide because ever since I took that class, I have learned how important it is to understand personal finance, and that especially for young working professionals, it is extremely important to start saving correctly right now. I am not claiming to be an expert (hardly one) in managing money, and you definitely should do your own research before doing anything. But I hope this is a guide that will help jump-start or help get you on track to managing your money right.

Magic of compounding#

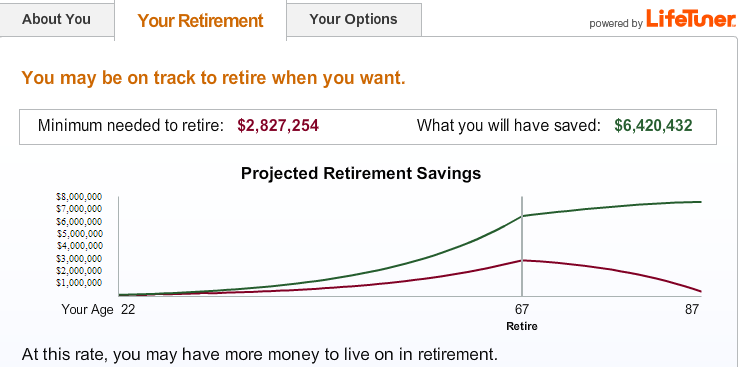

First step, think about retirement. My favorite retirement calculator is the AARP Retirement Calculator. It is the most simple and concise calculator to get you to start thinking about how much money you want to be saving in order to reach your goals when you retire. For me, it claims that I need a minimum of $2,827,254 to retire in the lifestyle that I want. However, based on my current savings trajectory (the amount I've saved so far and the amount I am saving on a monthly basis), I am estimated to have saved $6,420,432 by the time I retire. I sure hope that is true, I'll check this article when I'm 67 to see if I actually met this target :P.

Look at that graph. You can see that saving early has its benefits of exponential growth (assuming the standard 6% rate of return on savings, 3% inflation, and no dot-com bubble), or for the programmers, it looks similar to a plot of O(n^2) time complexity for bubble sort (until you hit age 67, which is when you get wiser and bubble sort becomes easier). As you continue to reinvest the money and put the money that you earn back into the account, the money compounds and that is what the magic of compounding is.

To give you a classic example, a fun question to ask a kid, "Would you rather have $10,000 per day for 30 days or a penny that doubled in value every day for 30 days?". Innocent and naive kids might choose the first option, but the correct answer is the latter option. The first option will net you $300,000 whereas the second option will net you over $5,000,000 dollars! Don't believe me? Here is the breakdown:

Day 1: $.01

Day 2: $.02

Day 3: $.04

Day 4: $.08

Day 5: $.16

Day 6: $.32

Day 7: $.64

Day 8: $1.28

Day 9: $2.56

Day 10: $5.12

Day 11: $10.24

Day 12: $20.48

Day 13: $40.96

Day 14: $81.92

Day 15: $163.84

Day 16: $327.68

Day 17: $655.36

Day 18: $1,310.72

Day 19: $2,621.44

Day 20: $5,242.88

Day 21: $10,485.76

Day 22: $20,971.52

Day 23: $41,943.04

Day 24: $83,886.08

Day 25: $167,772.16

Day 26: $335,544.32

Day 27: $671,088.64

Day 28: $1,342,177.28

Day 29: $2,684,354.56

Day 30: $5,368,709.12

That, is the magic of compounding. Time is on your side when you are young. Start saving now and see a greater return on your savings when you are older. When you are 70 years old and looking back, you can thank me for being able to retire on that private island of yours with your yacht (hopefully you'll hook me up and let me join you).

Why is time important? Take this same example, but say little Jimmy procrastinated and decide to start 10 days late into the 30 day trial. What if you had the right idea, but decided to just start a little later? Here's what happens, Jimmy experiences the same growth and numbers but he stops at day 20 (analogous to how we all will retire around the age of 65ish). Jimmy's penny is now worth about 5 thousand dollars compared to the other guy who started early and managed to net 5 million dollars with the same exact penny but started 10 days earlier. Jimmy would be furious and regret that he didn't take action earlier. Don't let that happen to you, seriously start now and don't be a Jimmy.

Are you convinced of the magic of compounding? Want to get started? Here is what I do and some tips and advice to get you started to a well deserved retirement.

Retirement#

401k vs IRA#

For retirement, you are usually looking at two options for where to store your money. The 401k and the IRA. Below, I'm going to talk about the differences and help you decide which one is better suited for you.

401k is a retirement investment vehicle provided by your employer whereas an IRA is something you set up on your own. Does your company match what you put in to a 401k? For example, if your company matches $.40 for every dollar you put in, up to 6% of your salary, that is free money and you should absolutely be contributing to 401k. In this example, the optimal amount to contribute is exactly 6% of your salary. If you earn $70,000 annually, put $4,200 (70000 * .06) every year into your 401k and you'll find that your company will contribute $1,680 (4200 * .40) of the company's money for free to your account. 401k is the way to go if your company provides some sort of contribution matching. For 2013, the maximum that you can contribute to a 401k is $17,500.

If your company matches 401k, then you should definitely do it. If not, then you can choose between 401k and an IRA. IRA offers more flexibility in terms of the different options that you can invest your money in, such as stocks, mutual funds and bonds. Do note that there are income limits which if you exceed, you cannot contribute to an IRA. Assuming you are under age 49, then the maximum that you can contribute as of 2013 to an IRA is $5,500. Note: it's not too late to contribute to your 2012 IRA! The deadline is April 15 so if you haven't done so, now is a good time to max out your 2012 contributions and then get started on your 2013.

401k and IRAs are retirement accounts, which means if you withdraw before you are of age 59.5 you will be slapped with heavy penalties and taxes except in a few exceptions. IRAs are a little more lenient in that you can withdraw early for a first time home purchase, education expenses or certain medical expenses. However, for the sake of brevity I won't go too deep into the various rules and penalties. Just keep in mind that the money you contribute into a 401k or an IRA is money that you should not plan on touching until you are verrrry old. You can see the various penalties here.

TL;DR: 401k if your company has a matching plan, IRA if your company doesn't because it is more flexible.

Traditional vs Roth#

Both IRA and 401k offer a traditional, and roth version and many people get confused and tripped up on what the difference is. The difference is that traditional means you don't pay taxes now but when you withdraw from your account (when you are retired), and roth means you pay taxes now, but not when you withdraw. So do you want to pay taxes now, or later? For young folks, it's been suggested that the roth type is the way to go because assumingly, you're in the lowest tax bracket right now so you should pay the tax now rather than later when you will be in a higher tax bracket in the future. Roth is a hedge against tax rates increasing in the future whereas traditional is a hedge against tax rates decreasing in the future. So the optimal strategy would be to have a balance of roth and traditional accounts to hedge against both scenarios. I really enjoyed reading this article and particularly the table that shows you all the possible scenarios (increasing tax rates vs decreasing tax rates vs equal tax rates in the future). I prefer roth because the penalty for early withdrawals are not as severe and the income limits are higher.

TL;DR: traditional means you pay taxes when you withdraw the money, roth means you pay taxes now but get to withdraw tax-free. Have a good balance of both to be optimal.

The importance of starting early to save for retirement#

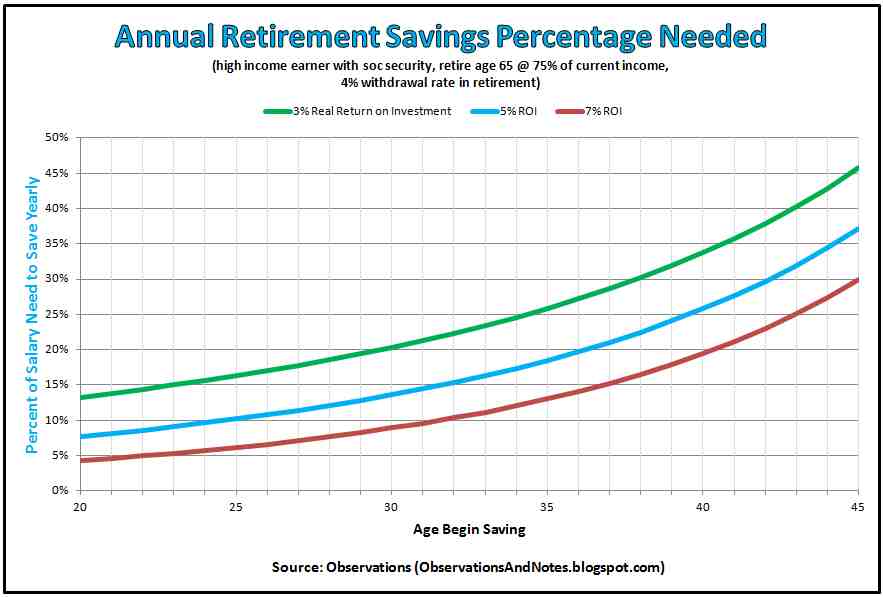

The younger you start saving for retirement, the less % of your annual salary you will need to save over time.

This graph is for high income earners (~100k/year) that I found from this blog that plots out the ideal % of your salary that you should be saving depending on what age you start saving for retirement. The different colored lines represent different amounts of return of investment. Realistically, you can just use the blue (5% ROI) since that's the average expected ROI for your retirement accounts. Notice that if you start saving for retirement at age 22, you only need to save about 10% of your salary towards retirement every year in order to live a comfortable life for retirement. If you want a baller retirement, then save more than 10%, I personally recommend 15%. That's really not too bad!

General Savings#

So we talked about setting up a retirement account, which is great. That money you contribute every year will pay itself off one day when you are retired and are unable to work anymore. However, there is a maximum cap to how much you can contribute to a 401k or an IRA. What about the rest of your money? Save it in a Bank of America savings account? Absolutely not - you will learn why in this section.

So in the previous section, we learned that a good amount to save for retirement is 10-15% of your salary. Where does that leave the rest of your money (that you don't spend on monthly expenses, food, and etc.)? If you save all your money in a savings account that has something like a <1% interest rate, then stop doing that immediately. Last year's inflation rate was 1.7% [source], which means if you store all your money in a savings account that earns less than 1.7% interest, that money in that account is actually decreasing in value year over year.

The recommended amount to store in these bank savings account is 3-6 months worth of living expenses. That measly interest rate savings account from now on, should be considered an emergency fund. This is what you tap into when you need money ASAP (e.g. emergency hospital, natural disaster, job loss, etc). Otherwise, the rest of your money should go into mutual funds and/or bonds.

You now have 15% of your salary going to retirement, you calculated what 3 months of living expenses is, and now there is a sum of cash that needs to go somewhere. This is where mutual funds and bonds come into play.

TL;DR: Regular savings accounts that earns <1% interest rate sucks. Leave only 3-6 months worth of living expenses in that account, and rest of your money should go to investments.

Investing#

Mutual funds are funds that are professionally managed that buy many securities such as stocks and money markets that are funded by people like you. For example, one mutual fund might focus on the US technology sector and thus their portfolio will have stock ranging from companies like Apple, Google, Cisco, and etc. The VITAX is actually exactly that mutual fund I'm describing. Each mutual fund comes with its own risk and restrictions. Things such as minimum investment, risk potential and expense ratios are all things you need to consider before purchasing a mutual fund.

You always want to invest in a mutual fund with a low expense ratio and that is because the expense ratio affects your returns significantly. For example, a mutual fund with a 1% expense ratio means that every year 1% of the fund will be used to cover expenses, which means less money to you.

In general, when you're young you can take more risk so having some investment in risky mutual funds is good. Bonds, on the other hand, is another investment vehicle which is low-risk but low return. A good rule of thumb is to have a portfolio that is X% bonds (X being your age), and 100 - X% in mutual funds/stocks. Which means that when you are young, you can be more risky and invest in mutual funds which are higher-risk but higher return. But as you get older, you should re-balance your portfolio to be more risk-averse and invest more in bonds and less in mutual funds/stocks over time.

TL;DR: Start an investment portfolio that is made up of X% bonds (X being your age) and 100 - X% in mutual funds/stocks. Take on more risk when you are young, and as you get older re-balance your portfolio using the formula in the previous sentence.

My Personal Finance#

I use Bank of America and Vanguard for managing my personal finances. My Bank of America saving's account only has about 1k for emergency situations (could use a little more here). Checking account is where my paycheck lands and where I keep my disposable portion of my income. 95% of my money is in Vanguard in the form of stocks, mutual funds, or IRAs.

I max out my Roth IRA account every year (so far only 2012), and with 2013 - I scheduled automatic transactions that withdraw immediately after my paycheck is deposited. It's spread out so that I will have deposited $5,500 into my 2013 IRA by the end of the year. I am currently using VTSAX for my Roth IRA because of the ridiculously low expense ratio (0.06%) and I am willing to take on the high-risk high-return nature of this fund.

I currently have some stock in FB as well (to play/learn about stocks), although I'm seeking to diversify soon because diversification is a good thing. In general, avoid independent stocks unless you really have the time and dedication to do the research and play the game. Mutual funds are superior for those of us who are more into the 'set it and forget it' mode because professionals manage mutual funds and is usually well diversified among many stocks.

Besides my automatic deposits to the Roth IRA, I am also contributing to the VTSMX mutual fund with it serving as my general savings account (I treat it like a savings account, except with much better "interest rate", 14% so far). However, I'm probably going to switch to a different fund that has a lower expense ratio that has a higher minimum investment in the future. VTSMX is a great fund to get started with.

Conclusion#

So that is pretty much it for my guide to personal finance for young professionals. If this guide was too long, here are the key takeaways that I hope you can remember:

- Start saving early for retirement. The earlier you start, the less amount (percentage wise) of your salary you have to save each year in order to live comfortably during retirement.

- Contribute to your company's 401k if they match, else open up an IRA. Always max these accounts out every year to the cap. Did I mention start early? Like right now?

- Aim for 10-15% of your income going to retirement.

- Only put 3-6 months worth of living expenses in your bank's savings account, the interest rate is usually abysmal and probably does not even beat inflation. Use it as an emergency fund for when you need money ASAP.

- For the rest of your money, put them in bonds and mutual funds. Follow the bonds/mutual funds allocation formula in the TL;DR of the "Investing" section above.

- Retire like a boss.

Hope this article has helped, and if there were any mistakes that I made, please leave a comment below so I can fix it. Anything I missed or was confusing? Let me know what you think!

But wait, there's more! An extra protip#

Here's an additional protip. If you have loans (e.g. student loans, car loans), should you try to pay those off first before saving your money in an investment portfolio? No, not always! Here's why.

Let's say your student loans have an annual interest rate of 4%. Let's be conservative and assume a 6% average annual rate of return on investments. In this scenario, you should not focus all your money in paying off the loans. Why? Because the investment return that you would receive is greater than the 3% that you lose out from interest, +2% to be exact. The optimal solution would be to put most of your money in investments, but still continue to pay off your loans albeit not as intensively. In the end, you will actually come out with more net worth because your investments will pay you back more than the amount you would have to pay in interest on the loan. If you are diverting all your extra money towards paying off the loan, you are actually theoretically coming out in a net loss (-2%) by trying to pay off your loans faster.

If the scenario was flipped, and the interest rate on the loan is higher than the average rate of return on investments, then you should definitely pay off your loans first before putting money in investments.

For example, my car loan has a 1.49% interest rate, and my VTSMX mutual fund which has been opened for almost a year, has seen a 14% return so far (of course, its only been a year and this year that can change), but as you can see, it is better to continue to put more money into the mutual fund to save rather than to pay off the loan faster because the ROI on the mutual fund is substantially greater than the interest I pay for the car loan. Currently, I'm aiming to pay off the car loan in 3 years so I pay the minimum amount every month to reach that goal. Nothing more, nothing less.

© 2024, Jesse Chen • d3be7b1